In a bid to make India a global hub for research and development (R&D) and to incentivize local innovation, the Indian government introduced Section 115BBF of the Income Tax Act through the Finance Act, 2016. This section provides a concessional tax regime for income earned through royalty from patents developed and registered in India. Let’s delve into the details of Section 115BBF, including its conditions, benefits, restrictions, and implications.

What is Section 115BBF?

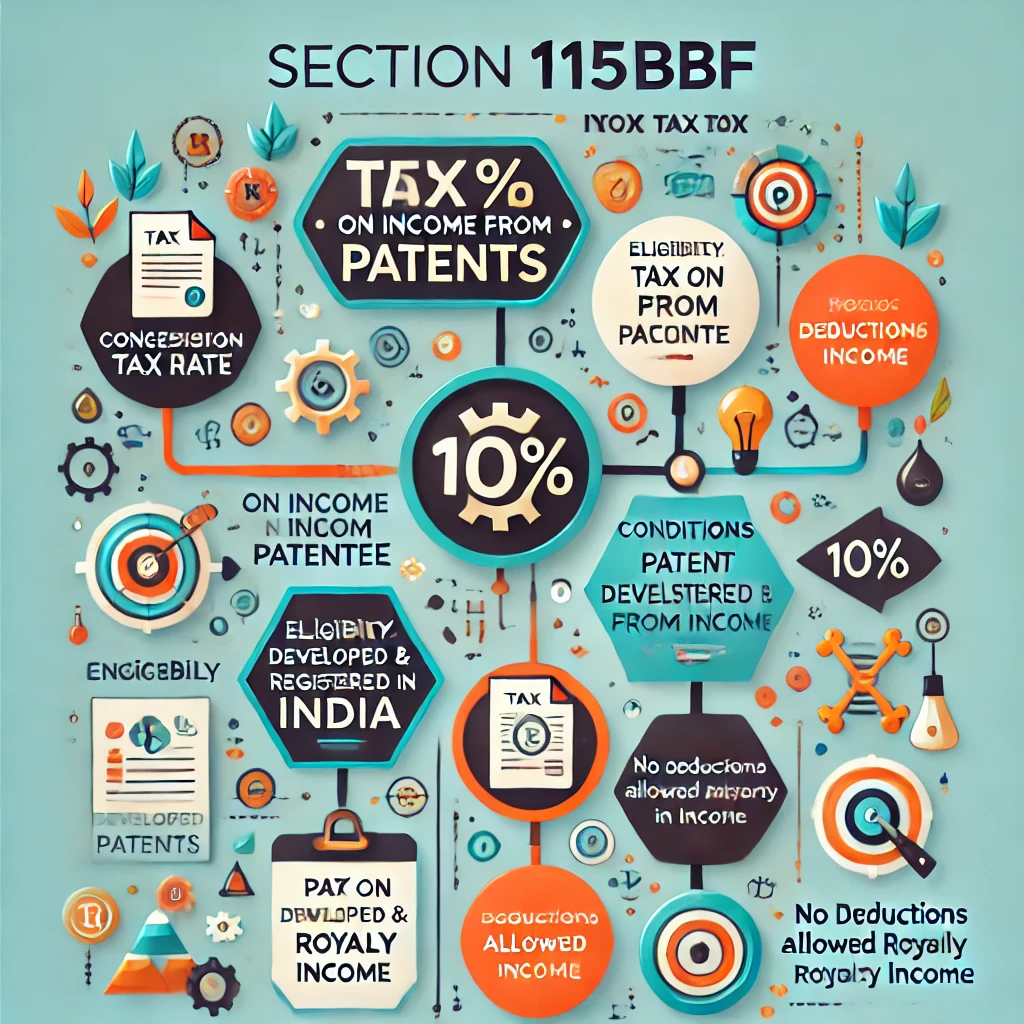

Section 115BBF of the Income Tax Act allows eligible taxpayers to opt for a concessional tax rate of 10% on income earned from royalties on patents developed and registered in India. This initiative aims to encourage indigenous research and patent development in India while providing a competitive tax environment for patent holders.

Key Features of Section 115BBF

- Concessional Tax Rate

- Royalty income from eligible patents is taxed at a reduced rate of 10%, which is significantly lower than the usual corporate tax rates.

- The tax liability for the taxpayer is calculated as the sum of:

- 10% of the gross royalty income, and

- Regular tax on the remaining income, excluding the royalty income from patents.

- Eligibility Criteria

- Resident Requirement: The taxpayer must be a resident in India to avail of the benefits under Section 115BBF.

- Patentee Definition: The eligible assessee must be the true and first inventor of the patent, registered as the patentee under the Patents Act, 1970. The section also covers scenarios where multiple individuals are registered as patentees.

- Development Requirement: At least 75% of the total expenditure related to the invention must have been incurred in India.

- Restrictions on Deductions

- Section 115BBF does not allow any deductions for expenses or allowances when computing royalty income. This restriction ensures that the concessional tax rate applies strictly to the gross royalty income, without any reduction for related expenses.

- Optional Regime

- Opting for the Scheme: Taxpayers can choose to opt for this concessional tax rate for any given financial year. The option must be exercised before the due date for filing the income tax return, as specified under Section 139(1).

- Consequences of Non-Compliance: If the taxpayer fails to follow the concessional regime in any of the five consecutive years after opting for it, the benefit of Section 115BBF will be withdrawn for the next five assessment years.

- Definitions under Section 115BBF

- Royalty: In this context, “royalty” refers to payments for:

- Transfer of rights or licensing related to the patent.

- Imparting information on the use or working of the patent.

- Usage of the patent.

- Services associated with any of the activities mentioned above.

- Invention: As per the Patents Act, an invention should be new, involve an inventive step, and be capable of industrial application.

- Patentee: The person listed as the first inventor in the patent register under the Patents Act.

- Royalty: In this context, “royalty” refers to payments for:

Conditions for Availing the Concessional Tax Rate

To be eligible for the 10% concessional tax rate on royalty income under Section 115BBF, the taxpayer must fulfill the following conditions:

- Patent Development and Registration

- The patent should be both developed (with at least 75% of the related expenditure incurred in India) and registered in India.

- Filing of Tax Returns

- The taxpayer must opt for the concessional tax rate while filing the income tax return for the relevant financial year, following the provisions of Section 139(1).

- Consistency in Opting for the Regime

- Once opted, the taxpayer must consistently follow this taxation regime for the subsequent five years. Failing to do so will disqualify them from availing of the benefits under Section 115BBF for the next five years.

Calculation of Tax under Section 115BBF

The tax payable under Section 115BBF is calculated as follows:

- Royalty Income Taxation

- The royalty income from patents is taxed at a flat rate of 10%.

- Tax on Remaining Income

- The regular income tax is calculated on the remaining income (excluding the royalty income) as per the general tax provisions applicable to the taxpayer.

- Surcharge and Cess

- Surcharge: The surcharge is levied according to the Finance Act applicable for the relevant assessment year.

- Health and Education Cess: An additional 4% cess is applied on the total tax amount, including the surcharge.

Benefits of Section 115BBF

- Encourages Indigenous R&D

- By offering a reduced tax rate on royalty income from patents, Section 115BBF incentivizes companies and individuals to invest in R&D within India, fostering innovation and technological growth.

- Boosts Global Competitiveness

- The concessional tax regime makes India an attractive destination for patent registration and development, potentially leading to more high-value jobs in R&D and technology sectors.

- Simplifies Taxation for Patent Income

- The fixed tax rate of 10% on royalty income provides clarity and predictability in tax planning for patent holders.

Limitations and Considerations

- No Deductions Allowed

- Taxpayers cannot claim any deductions for expenses or allowances related to royalty income under this section. This provision ensures that the concessional tax rate applies strictly to the gross royalty income.

- Five-Year Lock-in Period

- Once a taxpayer opts for the concessional tax regime, they must consistently offer the royalty income for taxation under Section 115BBF for five consecutive years. Non-compliance results in the loss of benefits for the next five years.

- Specific Applicability

- The section only applies to patents developed and registered in India, limiting its applicability to inventions with substantial R&D activity conducted within the country.

Recent Amendments and Updates

The concessional tax regime under Section 115BBF has been in effect since April 1, 2017, applicable from the assessment year 2017-18 onwards. There have been subsequent updates to the surcharge and cess rates over the years. Currently, the health and education cess rate is set at 4% on the total tax, including the surcharge.

Frequently Asked Questions (FAQs)

- Who can avail of the benefits of Section 115BBF?

- Only residents of India who are patentees can avail of the benefits under this section. The patent must be developed and registered in India.

- Can deductions for expenses related to patents be claimed under Section 115BBF?

- No, deductions for any expenses or allowances related to the royalty income cannot be claimed under this section.

- What happens if a taxpayer does not comply with the concessional tax regime for one year?

- If the taxpayer does not offer the royalty income for taxation under Section 115BBF for any year within the five-year lock-in period, they will lose the benefits for the next five years.

- Is the concessional tax regime mandatory for all patentees?

- No, opting for the concessional tax regime is optional. Taxpayers can choose to follow the regular tax provisions if they prefer.

Conclusion

Section 115BBF of the Income Tax Act is a significant step toward encouraging innovation and making India a global R&D hub. By providing a concessional tax regime for income from patents, the section aims to incentivize patent development and commercialization within the country. However, taxpayers must carefully evaluate the eligibility criteria, restrictions, and conditions before opting for this regime.

For more information on various sections of the Income Tax Act and tax planning strategies, visit Smart Tax Saver.